Prior to securing any mortgage, there are steps that must be taken. First, you need to know how to go about obtaining a loan for your home. That starts with this article and all the tips that are going to start you off the right way.

Have your documents carefully collected and arranged when you apply for a loan. You will realize that every lender requires much the same documents when you want a mortgage. Make sure you have items such as W2s, bank statements, income tax returns, and the last two pay stubs. Getting these documents together will make the process smoother and faster.

If your loan is denied, don’t give up. Instead, check out other lenders and fill out their mortgage applications. Every lender has different criteria. This is why it’s always a good idea to apply with a bunch of different lenders to get what you wanted.

Government Programs

There are some government programs for first-time home buyers. There are often government programs that can reduce your closing costs, help you find a lower-interest mortgage, or even find a lender willing to work with you even if you have a less-than-stellar credit score and credit history.

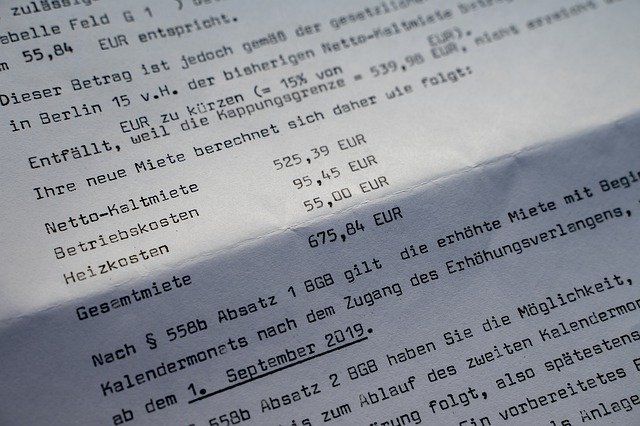

Go through your loan documents and make sure you understand every fee. This ought to encompass closing costs and other fees. Most companies are honest about the fees you will have to pay but it is always best to ask about fees before entering a contract.

When mortgage brokers are looking at your credit report, it is more beneficial to have low balances on several different accounts than it is to have a large balance on one or two credit cards. Your balances should be less than 50 percent of the credit limit on a credit card. It is best if your balances total thirty percent or under.

Always research your potential lender before making any final decisions. Don’t just trust in whatever they tell you. Try finding other clients who have used his lender. Look around the Internet. Check out the BBB. Know all that’s possible so that you’re able to get the best deal possible.

Once you have your mortgage, start paying a little extra to the principal every month. This lets you repay the loan much faster. For instance, paying an additional hundred dollars every month that goes towards principal can shrink repayment by many years.

Look beyond just banks. You may be able to save a lot of money if you have a relative that could lend you the money to buy a home. There are also credit unions that usually have much better interest rates. When you are searching for a mortgage, consider all your options.

Learn how to detect and avoid shady lenders. Though many are legitimate, others are unscrupulous. Don’t fall for fast talkers. Unnaturally high rates are a red flag, so do not sign any papers. Never believe anyone who says your bad credit isn’t an issue. Never use a lender who suggests you report your information inaccurately in order to qualify.

If there are issues associated with obtaining a mortgage from either a bank or a credit union, you may want to consider contacting a mortgage broker. Many times a broker is able to find a mortgage that will fit your circumstances better than traditional lenders can. Brokers work with a multitude of lenders, and are able to direct you to the optimum deal.

Make sure that your savings are abundant prior to applying for your first mortgage. It will look good on your balance sheet, but you may also need some of that money. You’ll need cash for closing costs, any points you may opt for, appraisal fees and other things. If you have a large down payment, you will have a better mortgage.

It is essential to keep your credit score good if you want to get the best interest rate on a home loan. Get credit scores from all the big agencies so that you can check the reports for errors. The score of 620 is oftentimes the cutoff these days.

Speak with a broker and ask them questions about things you do not understand. It’s important to understand everything involved in the process. Be sure and leave all your current contact information with your broker. Look at your email frequently in case they need certain documents or updates on new information.

Once you receive loan approval, it’s important to keep your guard up. Do not do anything that could negatively affect your credit until your loan is fully closed. The lender will probably check your score right before closing. A loan can be denied if you take on more debt.

Now that you have the information you need, don’t wait to get started. Use what you learned and get the ideal mortgage for your specific situation. Whether it is a first or second mortgage, the knowledge is now in your hands to find the very best offer for your family.